Create a free account or login to access more of investoguru.com

Create a free account or login to access more of investoguru.com

REGISTER NOW OR LOGINCreate a free account or login to access more of investoguru.com

REGISTER NOW OR LOGINThe world has more hungry mouths to feed every day. Ensuring food security for over seven billion people is already a huge challenge for farmers, especially with depleting natural resources, shrinking arable land, declining yields, increasing post-harvest waste and rising crop losses.

Global population is likely to touch 9 billion by 2050 and 11 billion by the turn of the century. Therefore, seeking sustainable solutions for crop security remains paramount.

The increase in population puts severe pressure on the land and the only way to feed the growing world is to enhance the Agriculture productivity with the total available total landscape.

During the covid, The agricultural activity has witnesses a huge growth and with a more than expected rains has aided

a better harvest and the industry which are associated with these are also witnessing a boom.

The Agro chemical Industry and they have been witnessing a boom in their sales and profitability in a time, where the economy is muted.

Agro chemicals are chemicals used to worldwide to elevate the Agriculture production, to control pests, diseases, weeds, and pathogens; and to reduce yield losses and all in all the Agro chemicals pay a pivotal role in enhancing the yield of the crop.

Though Agro chemicals has its own set backs in terms of the impact that it has on the soil and the toxic content of it makes it a concern but then it has taken its inevitable position in the Agriculture Industry.

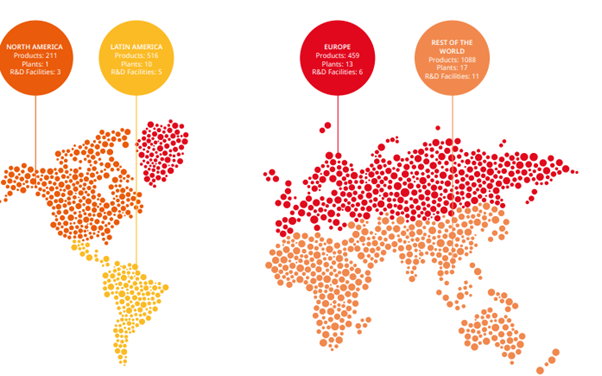

UPL is the 5th largest Agro chemical company in the world and world’s 4th largest seed manufacturing company. UPL has its presence across 138 plus nations which includes USA, Europe, Latin America, India many more. The company has 44 manufacturing facilities spread across the world.

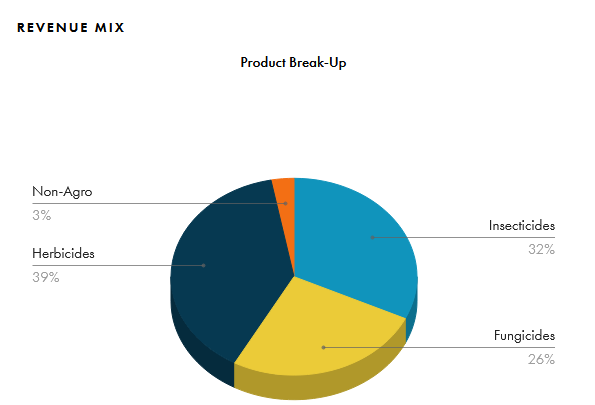

UPL has diversified its portfolio across fungicides, herbicides, insecticides, plant growth regulators, rodenticides, specialty chemicals, nutri-feeds, seeds and seed treatment products, postharvest solutions and industrial chemicals.

The company derives 80% of the revenue from the sales of branded products and the company has more than 13600 kinds of products to offer to its customers across the world.

UPL was promoted by R.D.Shroff (who is also current Chairman and Managing director) in 1969, and with a successful track record of more than 50 years in the Industry. UPL, over the last 25 years, has made 40+ acquisitions and been successful in accelerating growth in a profitable manner. The strategy adopted by UPL to enter into new geographies or new products, is to acquire companies which are already present in the segment and have a significant market presence.

A strong management is a like cushion to the investors, it absorbs all the shocks and threats that might arise in the future and a shrewd management has transcended many of the global issues through sheer insight.

Crafting new pathways through innovation:

Agriculture is a risky business, just like the solution, the problems also evolve through time. The profitability in this industry is closed revolved to how efficiently can the product tackle the various problems that arise on a day to day basis.

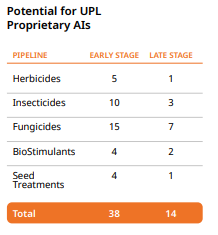

UPL has always committed itself a growth ushered through innovation. The company has been creating one of the world’s leading R&D facilities in the industry, leveraging its research capabilities, along with our strong complementary formulation development expertise.

The company has 26 R&D facilities spread across the world and the company has been granted more than 1266 patents.The company spends 2.3% of its sales value towards R&D and which has aided the company to attain the market leadership position across various product ranges.

The company had one growth strategy and that is to fuel the growth by Acquiring the companies which has established network across various nations and this strategy had a multiple advantages and that has indeed been a successful weapon for the company but then things started to change when the company went out make a costly purchase.

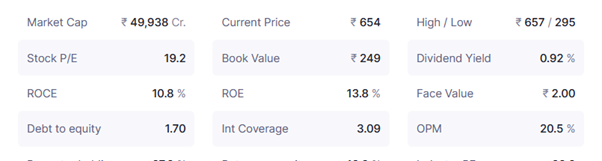

In the FY -2019, UPL acquired Arysta life science for 4.2 Billion dollars and even for a big company like UPL, it was indeed a big company and this purchase increased the debt levels of the company and the borrowings of the company stood at 32,750 crores as on Sep 2020, with a Debt to equity ratio of 1.70%

Now the unsolved mystery is whether this was a strategic acquisition or a costly mistake made by the company.

Any introduction of formulations and generic active ingredients might get postponed because undue extension of patent terms by the regulatory authorities which will directly impact the business of the company and any change in Government policies pertaining to agriculture is also a risk associated with the company.

UPL sells its products in more than 138countries across the world (through more than 90 subsidiaries) and it has production units spread in 48locations. Considering the nature of the product usage, registration, consequent environmental impacts, etc., UPL is required to comply with various local laws, rules and regulations and operate under strict regulatory environment.Further, there is always a risk associated with ban being imposed on pesticides as they may pose risk to human health.

Cyclical Business:

The company’s profitability is determined by the success of the Agriculture and the fate of the Agriculture is in the hands of Monsoons.

Thus, the relative boom is the Agro chemical business can change in a doom for the company due to a bad monsoon and which can change the fate of the company. This equation makes the business cyclical in nature and the company can bleed the most during the correction phase due to the elevated debts.

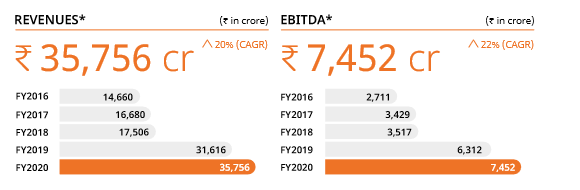

The Revenues of the company has witnessed a 20% CAGR in the past 5 years and the EBITA has also growth along with the Sales, which indicates that the company has been successful maintaining its profit margins for over the past 5 years.

The company is trading at a Price multiples of 19x, where the Industry PE is around 23x and the stock is trading 2.63 times of the book value. UPL is the market leader in the Indian Agro chemical business in terms of Market capitalisation.

The companies Debt remains at the elevated levels and that remains as a major concern about the company and the company has laid down plans to reduce the same in the days to come.

With one foot in the Emerging markets and the other one on the Developed nations, the company is sweet spot between the scale and agility. The company has surmounted all the inevitable challenges and has indeed made a rich legacy but, in the days, to come, the company should ensure that it’s own growth strategy doesn’t come back to bite its own tail.

share your thoughts

Only registered users can comment. Please register to the website.