BLS International Services Limited: Cost Management and Competitive Strengths Should Drive Next Leg of Growth

Summary

- Asset light business model of BLS International Services Limited supports on focusing better returns and efficient capital utilization.

- The company is a cash accretive business, with projects entailing direct collections from its customers.

- Sound credit measures and global presence should act as principal growth accelerators.

About BLS International Services Limited

BLS International Services Limited is a trusted global tech-enabled services partner for governments and citizens and is categorised amongst top 3 global players. It is a preferred partner for embassies and governments across world, with impeccable reputation for setting benchmarks in domain of visa, passport, consular, e-governance, attestation, biometric, e-visa and retail services. The company is also into providing citizen services to state and provincial governments. These services are offered across Asia, Africa, Europe, South America, North America & Middle East. This is only company in its domain with listing in India on NSE, BSE, and Metropolitan Stock Exchange of India Ltd.

Growth Enablers of BLS International Services Limited

- Efficient Cost Management Should Support Long-term Growth: BLS International Services Limited saw operational revenue of ~INR150.4 crores, exhibiting 14.6% growth quarter-over-quarter and decline of 26.4% on year-over-year in 3Q21. This decline was principally led by fall in visa processing services business. Fall in revenue impacted the company’s gross profit and EBITDA, but it has realigned expenses in line with business operations, minimizing decline in margins even though there was a revenue decline. The company started accepting appointments for visa applications for Embassy of Brazil in China from Dec 7, 2020. Five-year exclusive contract from embassy makes it necessary for the company to operate 15 centers across China. The company should be able to process 4,00,000 applications during this contract.

- Competitive Strengths Should Enable Sound Growth: The company’s agile, secure and highly scalable systems and processes should lend some support to business success. It ensures about data security through personal and cloud-based platforms. BLS International Services Limited has a strong global presence, with the company having branches in 62 countries and total 2325 centers globally in FY20. It should enable the company maintain dominant position in industry and should also result in capitalizing on growing business opportunities. The company has an asset light, high FCF business model. The company’s capital utilization mechanism focuses on using funds only for contract execution. Its citizen service offices are being operated by BLS and developed by government, which ensures optimization of costs.

- Focus on Long-term Growth Objectives: Through leveraging domain expertise, there are plans to continue focus on offering tech-enabled citizen services for governments and diplomatic missions worldwide. The company targets international market for outsourced citizen and front-end services. There are plans to take up government projects in India to accelerate future growth. BLS International Services Limited focuses on deepening presence through offering more services and improving wallet share. The company plans to enter new geographies so that emerging opportunities can be exploited. To track rapid digitization, the company focuses on leveraging advanced technology and its expertise to develop robust, agile and cutting-edge processes, enabling penetration and improved service experience. BLS International Services Limited plans to eye projects entailing direct collection from customers, eliminating dependency on government revenues and receivable cycles. Focus on asset light business model should be maintained with target of minimum capex for new projects, ensuring balance sheet strength.

- Capitalising on Sectoral Opportunities: The company plans to capitalize on global opportunities as most services being offered by governments to consumers are semi-automated, leading to low penetration of cutting-edge technologies. This results in slow and inefficient delivery. Outsourcing to specialized partner should result in reducing delivery time, increasing efficiency and customer delight. This enhances image of government and national brand, enabling win-win proposition for government both from cost font and service quality front. Plans are there to capitalise on domestic opportunities and there are number of initiatives by Indian government providing attractive opportunities in e-service domain. Government leverages solutions and services from specialist service providers, enabling them to realize vision of Digital India. After success of Punjab citizen services project and Starfin, BLS International Services Limited has seen new avenues of growth open up. While other states plan to replicate Punjab model to enable greater efficiency in government processes, the company should be able to reduce delivery times and enhance productivity. Global citizen services space remains yet to be explored. In absence of large-scale organized player, the company should be able to deepen its reach in this opportune field.

- Increased Global Presence and Technology Should Lend Growth: BLS International Services Limited is preferred customer as a result of its financial position, strong technical infrastructure and its ability to give maximum data security with help of personal and cloud-based platforms. Its agile, secure and scalable systems and processes should continue to stem business success. With expansion of its global presence, the company is being counted as a big player in visa processing & tech-enabled services. BLS International Services Limited increased its market share in outsourcing visa applications as it got an exclusive contract from Spain government and India mission. Apart from contract from Punjab government, wins from Canada & Egypt government should result in improved contribution from tech-enabled services vertical.

- Strong Financial Risk Profile- A Silver Lining: The company’s established market position should continue to lend support. To successfully overcome challenges and reduce impact on financials, the company has optimized costs and rationalized rent and operational expenses.

It has strong cash and healthy bank balance of ~INR240 crores and it should be able to address business requirements with sufficient cash flow. Asset light business model stems better returns and enables sound capital utilization. Besides, the company’s projects entail direct collections from customers, which makes it a cash accretive business. Sound credit metrics should help the company achieve reasonable growth.

- Industry Overview: Each and every industry and government face digital disruption across globe. Goal of government to citizen services is to offer one-stop, online access to information & services to citizens, enabling them to find and access what they need. Presently, services provided by government are semi-automated, having a low penetration of cutting-edge technologies. This led to increased demand for outsourcing to specialized partner, reducing delivery time. Government to citizen services market is developing at a rapid pace because of increased use of data, increased business collaborations and government regulations.

- Improved and Sustained Market Presence: The company’s contract with Spanish mission allows it manage 122 citizen and consular service centres in and across 47 countries. It has scaled its presence in Russia and China, with establishment of 28 centres in Russia and 15 in China on behalf of Spanish mission. The company started Vietnam visa application centre in Turkey, Brazil Visa application centre in Lebanon. Apart from this, it has started Morocco Visa application centre in India.

Conclusion

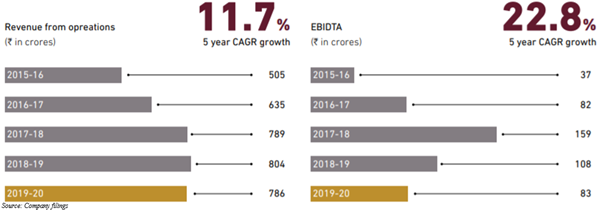

BLS International Services Limited has compounded its revenue at ~11.7% and its EBITDA at ~22.8% over 5 years. FY20 was a dynamic year for the company and it continued to strengthen focus on customer experience, technological investments and portfolio of offerings. These measures play pivotal roles to sustain market position as leading visa processing and tech enabled government to citizen services company. With world struggling with global pandemic, visa and consular services in countries such as China and Russia were suspended from early part of 4Q20. In some other countries, operations were completely stopped by Mar end. BLS Kendras in India were not operating during ensuing lockdown.

The company remained on track to deliver strong performance during initial three quarters of FY20. COVID-19 impacted revenues in 4Q20 due to countrywide lockdown. In FY20, BLS International Services Limited saw revenues of INR786 crores in comparison to ~INR804 crores in FY19. EBITDA was INR83 crores and PAT was INR52 crores in FY20. With economic activities picking up and removal of restrictions, the company’s stock price delivered strong returns.

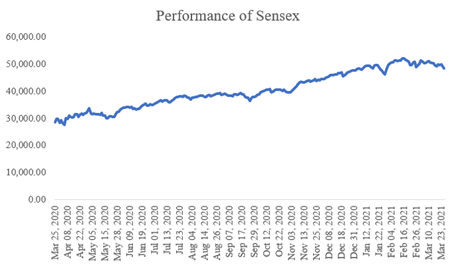

Between Mar 25, 2020-Mar 25, 2021, its stock price saw an increase of ~220.74%. This strong growth in stock price principally stemmed from improvement in operational revenue and steps taken to manage margins. An investor who would have invested INR1,00,000 on Mar 25, 2020, would have seen capital grow to ~INR3,20,741.57 on Mar 25, 2021.

In comparison to Sensex, the company’s stock price has performed very well. While opening up of economy was celebrated by Sensex also, index was not able to defeat returns delivered by BLS International Services Limited. Between Mar 25, 2020- Mar 25, 2021, Sensex has delivered only ~69.75%.

Exclusivity:

This article is exclusive to investoguru.

Stock Disclosures:

The author has no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Author Disclosures:

This Article represents the Author's own personal views. The Author did not receive any compensation and do not have any business relationship with any of the companies mentioned in the Article.

share your thoughts

Only registered users can comment. Please register to the website.